Working Papers

Pre-Trends Ahead of Monetary Policy Surprises: Recovering the Response of Corporate Investment

with , ,

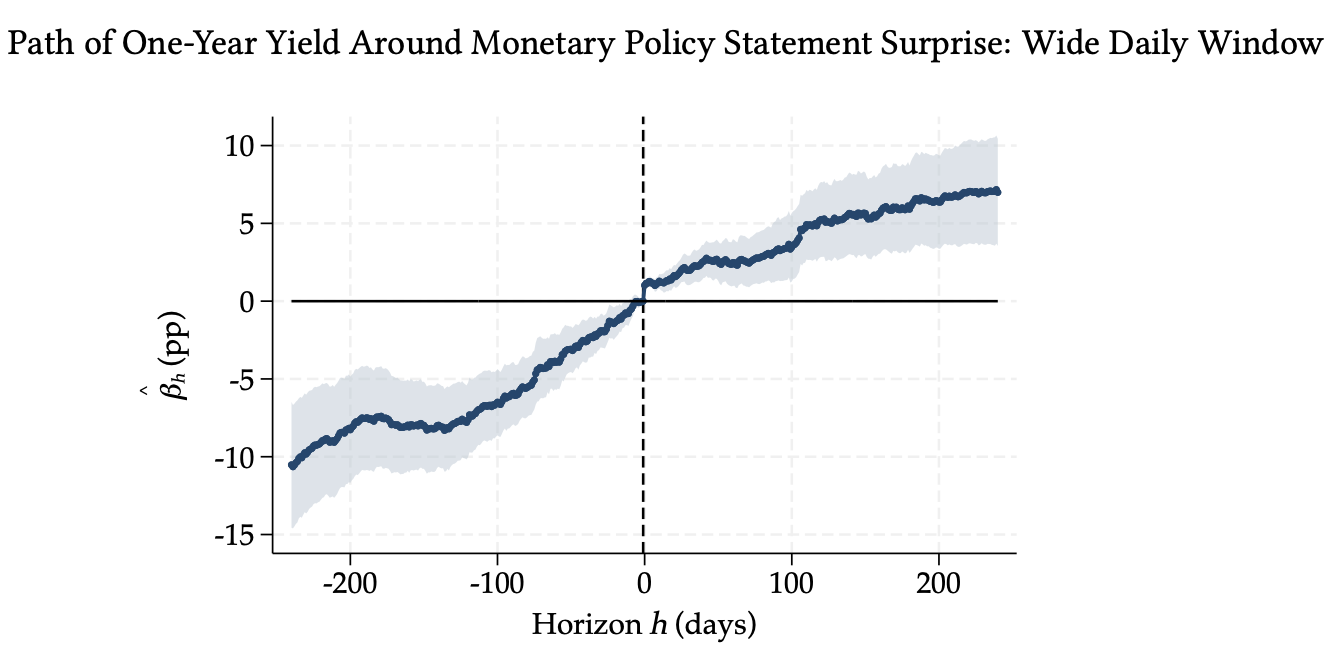

Abstract: How should high-frequency monetary policy surprises be used when the outcome of interest is only observed at a lower frequency? We first document a business-cycle endogeneity problem that arises when monetary policy surprises are aggregated to monthly or quarterly frequencies—surprise policy easings (resp. tightenings) tend to occur amid broader easing (resp. tightening) cycles. These low-frequency trends in pre-event Treasury yields are not reliably removed by standard controls without also weakening the relevance of the remaining policy variation. Motivated by this evidence, we next develop an alternative Q-theory-based approach for estimating the corporate investment response to monetary policy. Our approach combines high-frequency identification of firms' valuation responses to policy surprises with low-frequency firm-level investment-Q sensitivities. Our baseline estimate is: a one-unit monetary tightening, normalized to a one percentage point increase in the one-year Treasury yield, reduces the annual tangible investment of non-financial, non-utility public firms by 0.38% of GDP, with 24% of this effect driven by a novel firm-heterogeneity channel.

Crowding Out Long-Term Corporate Investment: The Role of Long-Term Government Debt Supply [SSRN] [Short Q&A]

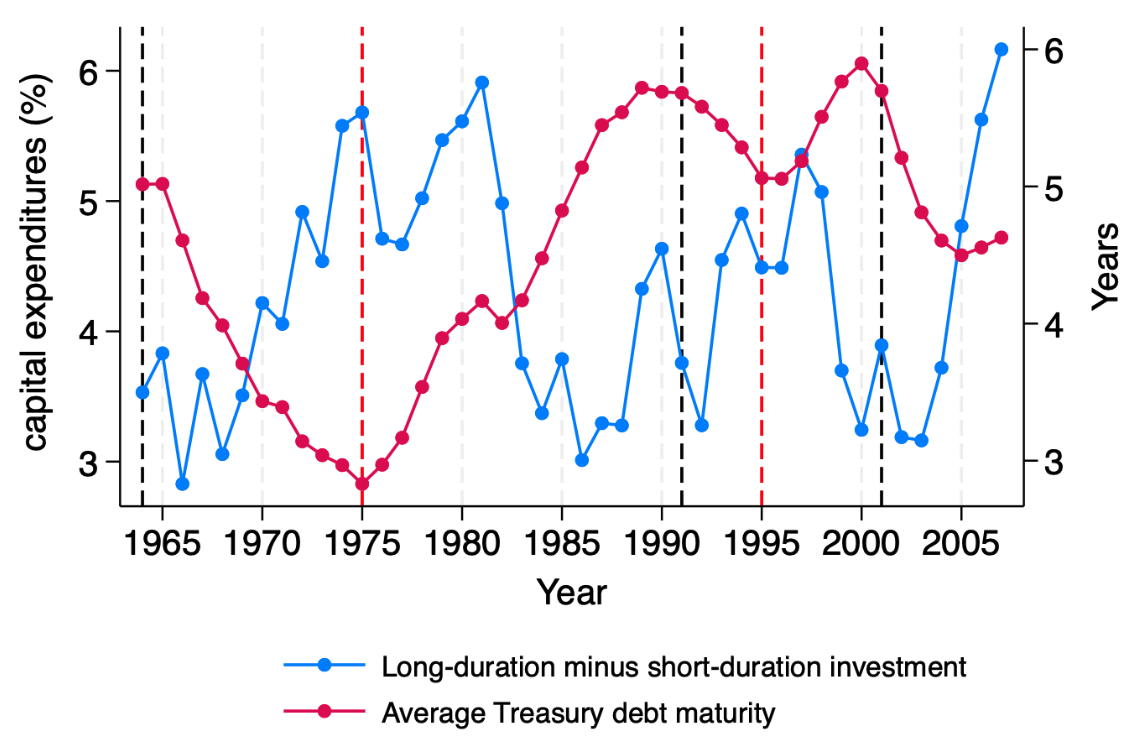

Abstract: Using large, plausibly exogenous shocks to the maturity structure of U.S. government debt, I provide the first causal evidence that the supply of long-term government debt affects the duration of corporate investment. I find that an increase in the supply of long-term government debt increases long-term discount rates, crowding out long-duration investment. This crowding-out effect reallocates capital from long-duration investment towards short-duration investment. This reallocation occurs across industries, within industries across firms, and within firms across divisions. I provide evidence that this reallocation depends on investment duration but is independent of firms' capital structure. Due to the prevalence of asset–liability maturity matching, the resulting variation in aggregate investment duration explains a sizable share of the variation in aggregate corporate debt maturity. My findings imply that policies which influence the net supply of long-term bonds, such as public debt management and central bank quantitative easing or tightening, affect the composition of corporate investment.

Selected presentations: European Summer Symposium in Financial Markets 2025, UIUC Gies, USC Marshall, Cornell SC Johnson, EIEF, LBS, LSE, MIT Sloan, UW-Madison, Chicago Booth, Notre Dame Mendoza, Wharton, OSU Fisher, Boston Fed, NYU Stern, Banque de France Empirical Corporate Finance Workshop 2024, Collège de France, EFA Doctoral Tutorial 2024, SFS Cavalcade 2024, Berkeley Haas, Columbia University, Chicago Booth Treasury Markets Conference 2024, AFA 2024, SED 2023, FIRS 2023, Adam Smith Workshop 2023, MFA 2023, FIFI Conference 2022, FIRS 2022 Ph.D. Student Session.

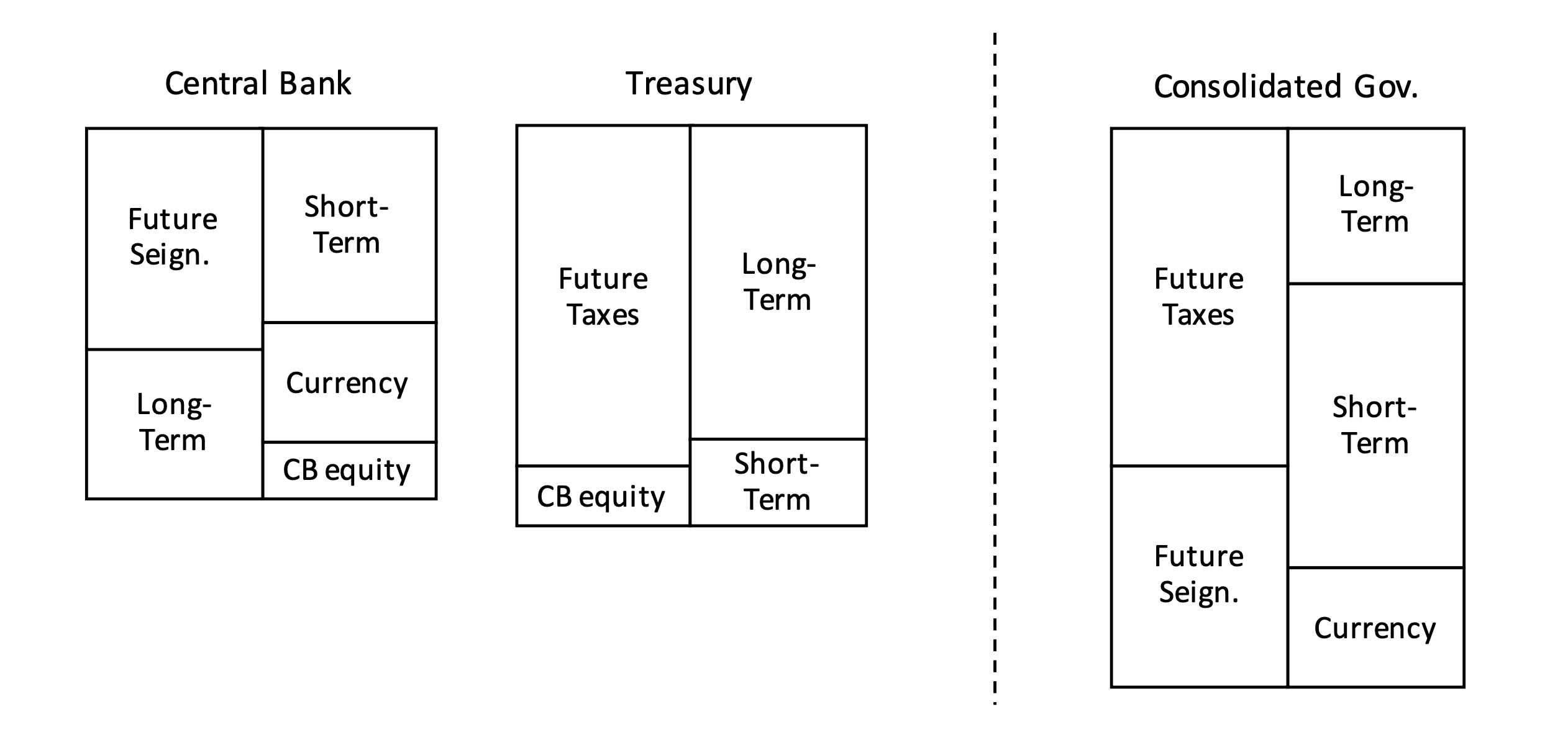

The Fiscal Cost of Quantitative Easing [SSRN]

with , ,

Abstract: Quantitative easing (QE) shortens the duration of the consolidated public balance sheet by swapping long-term government bonds for short, floating-rate liabilities, thereby shifting interest-rate risk onto taxpayers. In segmented bond markets, absorbing duration from the marginal investor can support real activity, but it also generates statecontingent losses that must be financed with distortionary taxes. We quantify the resulting ex ante fiscal-efficiency cost by forecasting QE-portfolio return distributions and mapping these into expected tax deadweight losses under a conservative terminal financing rule. Across all recent U.S. QE programs, the expected costs total 0.35% of GDP under risk-neutral valuation and 1.35% of GDP as a conservative upper bound. At origination, published estimates of QE output effects exceed our estimated fiscal-efficiency costs for each U.S. QE program.

Selected presentations: Cesifo Macro, Money, and International Finance 2025, WFA 2025, Oxford Saïd-VU SBE Macro-Finance Conference 2025, SFS Cavalcade 2025, Adam Smith Workshop 2025, BEAR Conference 2025, GRETA Sovereign Bond Markets Conference 2025, USC Macro Finance Conference 2025, Stanford SITE 2024.

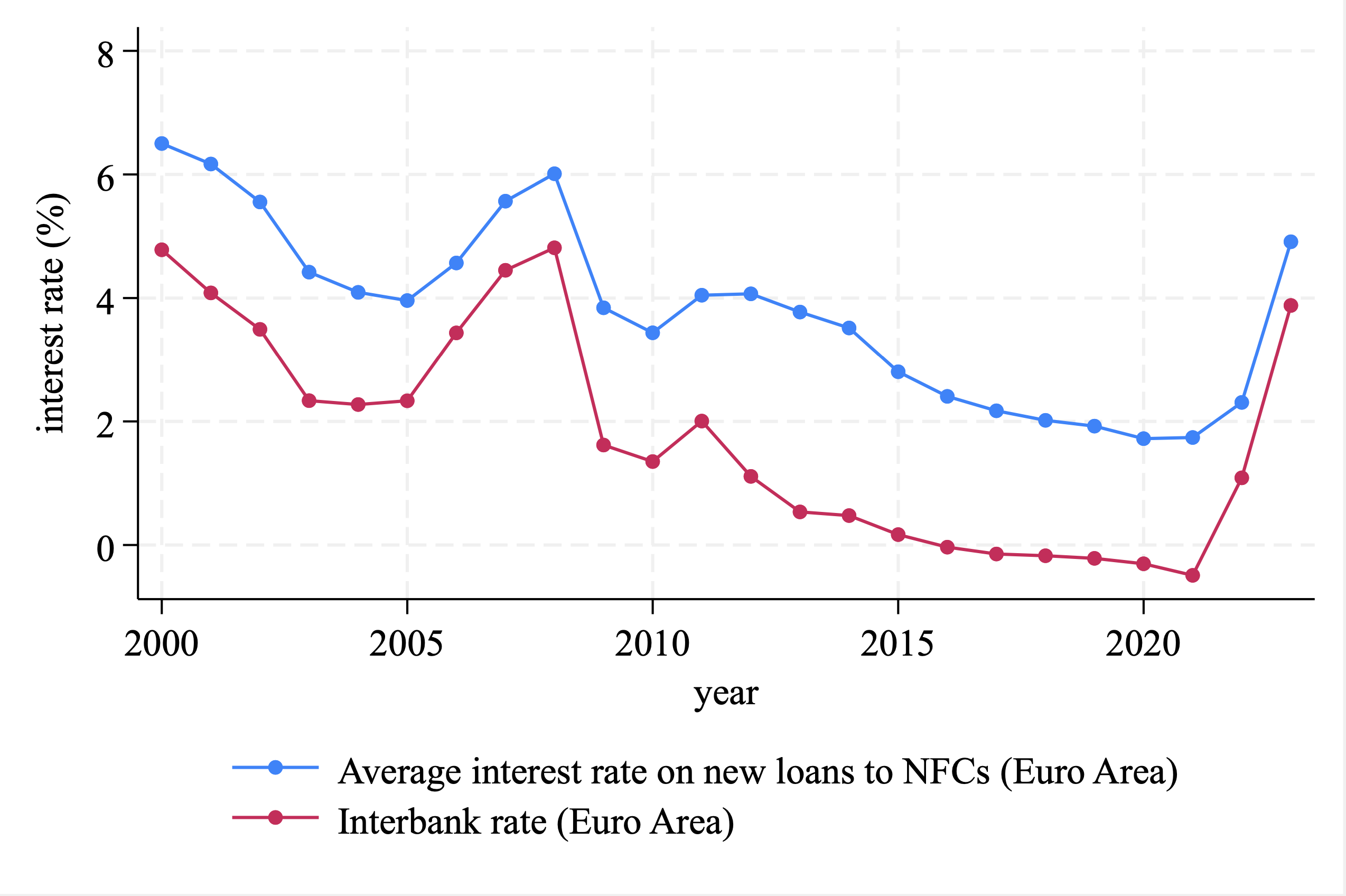

Loan Spreads and Interest Rates: The Role of The Deposit Channel and Lending Market Power

with

Abstract: We present evidence that loan spreads earned by banks over marketable interest rates are, in the French business lending context, inversely related to the level of short-term interest rates. Controlling for the pricing of credit and interest rate risks, we show that this negative correlation is consistent with a credit supply shock: banks who increase loan spreads more when interest rates decline also experience lower growth in credit supply. We find empirical support for theories that link frictions in the deposit-taking business to lending outcomes of financially constrained banks. Lower rates compress deposit spreads earned by banks, prompting constrained banks to reduce lending, and explaining the rise in loan spreads. We also find support for a complementary channel, lending market power. Specifically, lenders with higher market share and borrowers facing a higher "hold-up problem" are associated with a lower interest rate pass-through. Finally, we provide novel evidence of negative real effects on corporate financing and investment for firms borrowing from banks with lower interest rate pass-through.

Selected presentations: SGF 2026, EEA 2025, FIRS 2025.